Life cycle costing is the process of assigning all costs that the owner of an asset will incur over its lifespan from acquiring the asset to get rid of the asset. These costs include the initial investment, operation and maintenance cost, cost of poor quality (COPQ) interest on investment, minus any salvage value at the end of life of asset.

Return on Investment (ROI) should be the criteria for evaluating the asset based on Life Cycle Costing (LCC) and Overall equipment Effectiveness (OEE) not merely on the capital cost and output parameter. Often capital investments are done considering the asset cost and the output parameters likes volumes / hour, but we forget to account for energy cost, environment impact cost, quality cost (COPQ) operation personnel cost, maintenance cost etc which are part of operational cost.

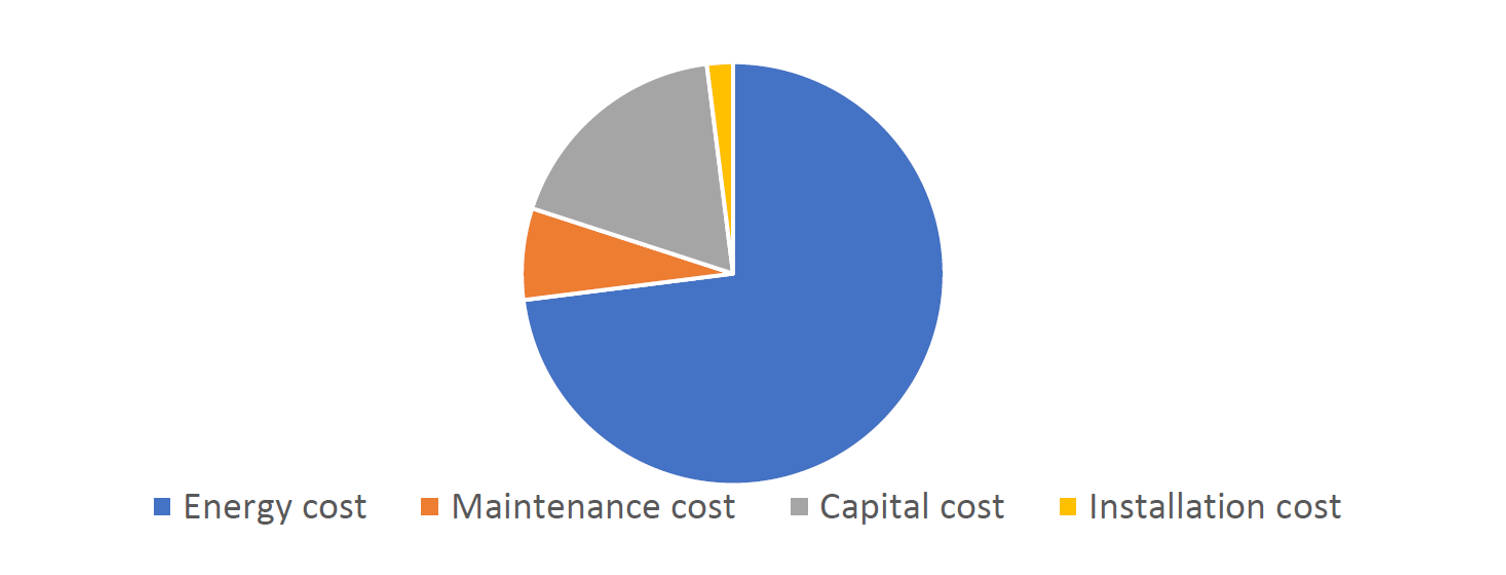

A study by Carbon Trust mentioned that for an Air compressor, a common asset used across industries for a 10-year life span the energy cost is 73%, capital cost is 18% maintenance cost is 7% and installation cost is 2%. So only basis of the capital cost and output without looking at the energy cost and maintenance could be a wrong decision.

Life Cycle Cost

Similarly, for industry asset OEE is very critical which is a KPI of plant productivity that bring efficiency to operation. OEE of an asset depends on the availability ratio (A), Quality ratio (Q) and performance ratio.

- Availability Ratio – The share of the actual production time and the planned production time. All planned stops and breakdowns will reduce the availability ratio, including set up times, preventive maintenance, breakdowns and lack of operators. The only time that you may choose to deduct from the availability ratio is lack of orders.

- Performance Ratio – Loss of production due to under utilization of the machinery. In other words, losses are incurred when the equipment is not run with full speed. Short, unregistered, stops may affect the performance ratio as well.

- Quality Ratio – The amount of the production that has to be discharged or scrapped.

All the three ratios are important for taking decision on LCC. Let us discuss each parameter in terms of LCC.

Availability ratio:

If the asset is on reliable, breakdown frequently may be due to hardware or software issue then the availability of the asset reduces to the planned run hours. This will impact the overall output planned Service support from the asset supplier is very important. Many a times it is observed that due to poor service support asset remains under unavailable condition to operation.

Performance Ratio:

When the asset is under utilized or when it is not run to its full capacity the performance ratio reduces and that impact the productivity.

Quality Ratio:

Asset are supposed to make 100% acceptable quality product but due to inherent design property they produce rejected product as well. The more the reject the less the productivity.

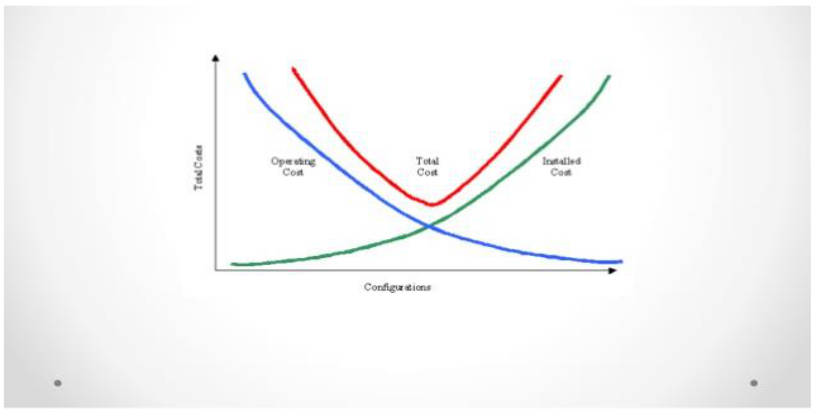

The Lifecycle Cost Curve

Let us take one example to understand the effect of OEE on LCC for an asset which is operating at 90% availability, Performance at 93% and quality at 91% verses a higher capital cost but better A, P&T of 95%, 98% and 97%.

OEE of Asset with Low capital cost A x P x Q = 0.90 x 0.93 x 0.91 = 0.76 (76%)

OEE of Asset with higher capital cost= A x P x Q = 0.95 x 0.98 x 0.9 = 0.83 (83%)

Therefore, we can see 7% improve in overall effectiveness or productivity which is substantial and should be considered as an evaluation criterion of asset.

The life cycle costing estimates help in the decision making process where the mutually exclusive option is available. As shown in the above figure it is a trade-off between operating cost and capital or installed cost of the asset. Also, the management can plan on how to reduce the overall cost of the item through the extension of useful life, efficient utilization, or other similar cost.